I personally find the people who are in the software startup game just for the money to often be nearly delusional about their chances of success and the likely magnitude of it when it happens. Before I get into the details for founders, let me talk about options-hungry employees. If you are in it for the money and you aren’t a founder, you’re sticking your head in the sand. Full stop. Yes, you can point at your anecdotal evidence at once-per-generation companies like Google, Amazon, and Microsoft. But for the most part, employees never get “I never have to work again” rich doing startups. There are too many mechanics out there to make sure that the folks taking the real risks (investors and founders) make the real money. If you want to read more, read my intro to startup stock options. If you don’t want to start companies, focus on salary and how much you enjoy working at startups.

But even if you are a founder, don’t do it for the money. Do it because you love small teams. Do it because you love your product. Do it because you love playing the startup game (even if you don’t win it). But for the love of God, don’t do it because you think you’ll get rich and retire on a beach somewhere when you’re 30. Because, as crazy as it sounds, when you sell your first company it almost certainly isn’t going to happen.

Let’s run through a common exit scenario. You and 2 co-founders spin up a company (say you’re creating one of Mike Arrington’s “Dipshit Companies that wants to sell to Google for $20m“). You take a smallish seed round and a small-ish Series A round (yeah yeah, you can bootstrap– but the vast majority of 7 to 9-figure exits are funded companies). So after investors and options for employees, let’s say you each own 20% of your company (it can be a lot less or more, depending on what kind of leverage you have while fundraising, how big your options pool is, and how many of those options are exercised/accelerated upon exit). Now let’s say you exit for $20m 3 years into it. Congrats! Light up the cigars and start hunting for beach houses– you’ve now joined the new rich! Except you really haven’t. You see, you (like a lot of folks) aren’t really thinking what it means to retire at 30. You’re not alone. The fellas at AdGrok have the same mental math going on in their head in their “Fuck You, Money” post:

“Before anything else, let’s do the numbers: money market funds yield around 4%. That’s $400K interest on $10MM, which is certainly a living wage, leaving aside inflation. Of course, it doesn’t have to last forever: human life is sadly finite. Crunching more realistic numbers, ‘fuck-you money’ is about $4.2MM for a 30 year old guy who plans on dying at 70 and wants to make $200K/year. Well within the payout picture of a fortunate startup founder whose company is acquired.”

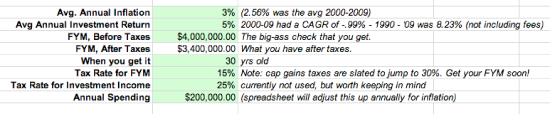

Of course, many of these numbers are strange. 4% for a money market? I’d love a link to that– the best I’ve been able to find is around 1.5% right now for a jumbo money market. Dying at 70? Chances are you’ll live to 90, at least. “Leaving aside inflation”? That’s disastrous (why would you leave aside a number that cuts your 4% by more than half?!). Let’s run through some REAL numbers, using my “Early Retirement Spreadsheet” (AKA “Fuck You Money Spreadsheet of DOOM” – feel free to save a copy and noodle with it).

In our above scenario, our happy founders are walking away with 20% of $20m, or $4m (might be a touch more due to unclaimed options, or a lot less if your investors are the double-dippin’). $4m– we could live on that forever, right? Let’s plug in some variables. 3% for average inflation (a touch higher than the average over the last decade to be conservative). Let’s assume you can get a 5% return (even though the last decade gave us -0.99% for the S&P and the outlook isn’t too rosy). And let’s assume you want to live in a major metro area in a nice house, a couple of kids in private school, and solid travel budget. You’re a millionaire, right? So let’s assume your annual family budget will be $200k. Upper middle class– certainly not in “butler country”, but real comfy, flying first class and living large. Here are our variables:

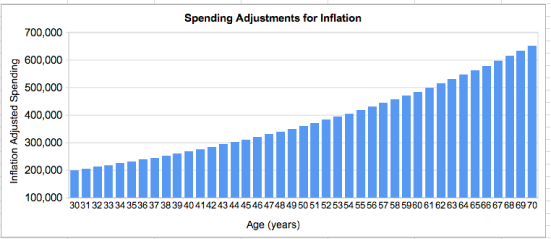

That’s not too crazy-conservative, is it? Heck, if you’re earning 5% on $4m, that’s $200k right there. No problem, right? You can coast forever with your fat nest egg largely untouched. You’re probably doing what I (and the AdGrok guys above) were doing: “Leaving aside inflation”. Let’s look at what you’ll have to spend to keep your $200k per year lifestyle with compounding annual inflation.

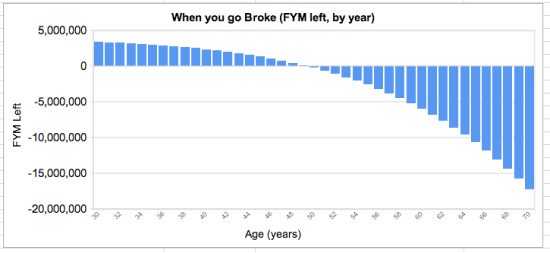

Wait a minute! I’m going to be spending nearly half a million dollars per year when I’m 60 to compensate for a 3% annual inflation? Don’t worry– you’ll be broke LONG before you 60th birthday. Let’s look at how your F@#$ You Money evolves over time with these variables.

You don’t even make it to 50. If you want to be optimistic about inflation and investment income (after all fees) and nudge them to 2.5% and 7% respectively, you don’t make it to 60.

There are a few morals to this story:

- make sure you freakin’ LOVE what you do. Love the game, love your product, love your co-workers, love your market.

- If you are going to be a mercenary, make sure to optimize not just for “f@#$ you money” but “f@#$ you influence”– make sure that as you sell your $20m company that you are well positioned to build another company, have a fat executive job, some great advisory roles, paid speaking engagements, and the like. Because you’re still going to want income.

- DON’T love the idea of living rich AND being retired. You can live rich on $5m OR you can retire early with $5m– but you sure as hell aren’t going to do both… for long.

Note: If you’d like to see the spreadsheet, it’s here. You can make a copy of it if you’d like to noodle with the variable to find your personal “never have to work again” number.